If you’ve ever found your inbox flooded with emails from TrueAccord, claiming you owe a debt, you’re not alone. The sudden surge in communications from this debt collection agency has sparked concerns and complaints from individuals questioning the legitimacy of the company’s debt collection practices.

In this comprehensive review, we delve into the intricacies of TrueAccord debt collection emails, scrutinizing user experiences, potential scams, analyze user reviews and complaints, and offering insights into how to navigate this financial landscape.

What is TrueAccord?

TrueAccord Corporation, based in San Francisco, CA, is a third-party debt collection agency founded in May 2013. The company employs a nearly fully-automated management system that utilizes machine learning to create personalized, digital-first consumer experiences.

This system tailors communications based on factors like frequency, timing, channel, and content. It primarily deals with delinquencies from credit cards, internet-based subscription services, consumer loans, e-commerce, and telecommunication accounts.

Consumer Complaints Reveals the Bitter Truth

Real user reviews and complaints paint a varied picture of True Accord’s practices. Some individuals report receiving emails for debts that are over 20 years old, with claims that these debts cannot be sued or reported due to their age. Others express concerns about receiving communications for debts they do not recognize or owe. These firsthand experiences raise questions about the accuracy and legitimacy of TrueAccord’s debt collection efforts.

One user, Brad W, expressed his distress on October 10, 2022: “I have received 23 emails from True Accord stating I owe $4,858.55 on a debt that is over 20 years old or more. The emails state: ‘The law limits how long you can be sued on a debt. Because of the age of your debt, LVNV Funding LLC cannot sue you for it, and LVNV Funding LLC cannot report it to any credit reporting agency.'”

Another user, Elijah B., had a concerning encounter on March 17th, 2023: “TrueAccord sent me an email about someone else’s account claiming it was mine. I had never heard of them or LVNV, who apparently turned the account over to True Accord. They are a fraud and should be put out of business since all they do is harass people like me, a senior citizen hoping to make money on stupidity.”

These real-life experiences raise valid concerns about the practices and accuracy of the company’s debt collection methods.

Is TrueAccord Debt Collector Legitimate or a Scam?

According to the Better Business Bureau (BBB), TrueAccord is a legitimate debt collection agency incorporated in Delaware in May 2013. The BBB file, opened on the same date as the company’s incorporation, lists True Accord with an estimated staff size of 10 people. It’s mission, as stated on their website, is to fundamentally change the debt collection industry by turning collections into a recovery and reconciliation process.

However, user comments raise doubts about the company’s legitimacy, leading to questions about its practices. While the BBB acknowledges TrueAccord’s existence as a legitimate business entity, user complaints and reviews suggest a more nuanced reality.

Elijah B., in his review, asserts, “They are a fraud and should be put out of business since all they do is harass people like me.” This sentiment is echoed by other users who feel harassed, confused, or even targeted by True Accord’s debt collection efforts.

Tips to Stop TrueAccord Debt Collection Harassments

Consumers have rights under the Fair Debt Collection Practices Act (FDCPA) to protect them from harassment and deceptive practices by debt collectors. If you feel harassed or misled by TrueAccord, you can take legal action and enforce your rights.

Understanding your rights is crucial in dealing with any debt collection agency, and True Accord is no exception. The FDCPA prohibits debt collectors from engaging in unfair, deceptive, or abusive practices. If you believe it has overstepped its bounds, you can take the following steps:

- Request Verification of the Debt: If you doubt the legitimacy of the debt, you have the right to request verification from TrueAccord. They must provide you with information about the debt, including the amount owed and the name of the original creditor.

- Cease and Desist Letter: You can send a cease and desist letter to the company, instructing them to stop contacting you. Once they receive this letter, they are legally required to cease communication, with a few exceptions.

- Dispute the Debt: If you believe there is an error in the debt amount or if you don’t recognize the debt, you can dispute it. Write a letter to TrueAccord explaining why you dispute the debt and include any supporting documents.

- File a Complaint: If True Accord continues to engage in harassing behavior, you can file a complaint with the Consumer Financial Protection Bureau (CFPB) and your state’s attorney general office.

It’s essential to keep detailed records of all communication with the company, including dates, times, and the content of conversations. This documentation can be valuable if you need to escalate the issue.

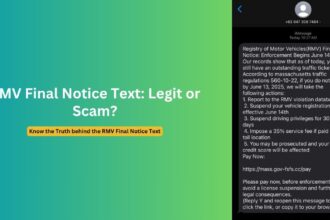

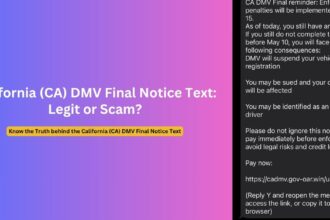

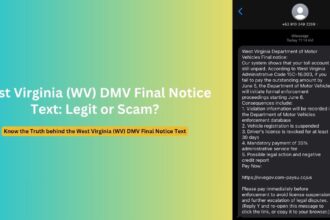

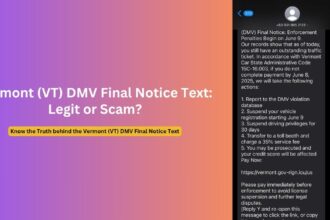

How to Stay Safe From Debt Collection Phishing Scams

Recognizing phishing scams in debt collection emails is crucial for protecting your personal information. Phishing scams often involve fraudulent attempts to obtain sensitive information, such as usernames, passwords, and credit card details, by posing as a trustworthy entity.

Here are some practical tips to help you identify and avoid debt collection phishing scams:

- Verify Sender Details: Legitimate debt collection agencies will provide accurate and verifiable contact information. Check the sender’s email address and cross-reference it with the official contact details of the debt collection agency.

- Validate Links Without Clicking: Hover over any links in the email without clicking on them to preview the URL. If the link seems suspicious or doesn’t match the official website of the debt collection agency, it could be a phishing attempt.

- Check for Spelling and Grammar Errors: Phishing emails often contain spelling and grammar mistakes. Legitimate businesses typically proofread their communications, so errors could indicate a fraudulent message.

- Research the Debt Collection Agency: Conduct online research to verify the legitimacy of the debt collection agency. Check customer reviews, ratings on the Better Business Bureau, and any reported scams associated with the agency.

- Be Cautious of Urgent Language: Phishing emails often use urgent language to create a sense of panic and prompt quick action. Be skeptical of emails pressuring you to make immediate payments or provide sensitive information urgently.

- Contact the Agency Directly: If you receive an email that seems suspicious, independently verify the debt by contacting the debt collection agency directly using the official contact information available on their website.

By staying informed and cautious, you can minimize the risk of falling victim to phishing scams and protect your personal information from unauthorized access.

What to Do If You Get Scammed

If you find yourself a victim of a debt collection phishing scam, swift action is crucial to mitigate potential damage. Here are steps you can take if you realize you’ve been scammed:

- Report the Scam: File a complaint with the Federal Trade Commission (FTC) through their online portal or by calling 1-877-FTC-HELP. Provide details about the scam, including the email content and any interactions with the scammer.

- Contact Your Bank: If you’ve shared any financial information, contact your bank or credit card company immediately. They can guide you on the necessary steps to protect your accounts and prevent unauthorized transactions.

- Update Your Security Measures: Change passwords for your email, bank accounts, and any other sensitive accounts. Enable two-factor authentication where available to add an extra layer of security.

- Monitor Your Accounts: Keep a close eye on your bank statements, credit reports, and any other financial accounts for any unauthorized activity. Report any suspicious transactions promptly.

- Educate Yourself: Learn from the experience to avoid falling victim to similar scams in the future. Stay informed about common phishing tactics and regularly update your cybersecurity practices.

FAQs

1. Are the emails from TrueAccord real or fake?

TrueAccord is a legitimate debt collection agency; however, user experiences vary. If you doubt the authenticity of an email, verify the sender’s details, and cross-reference with it’s official contact information.

2. What should I do if I receive emails, texts or calls for a debt I don’t recognize?

If you receive emails, texts or phone calls for a debt you don’t recognize, request verification from the company. They are obligated to provide information about the debt, including the amount owed and the original creditor’s name. You can also check your credit report and if you don’t find of that unknown debt then ignore them.

3. How can I report harassment or deceptive practices by TrueAccord?

If you believe TrueAccord has engaged in harassment or deceptive practices, document the incidents and file a complaint with the Consumer Financial Protection Bureau (CFPB) and your state’s attorney general office.

4. What rights do I have under the Fair Debt Collection Practices Act?

The FDCPA protects consumers from unfair, deceptive, or abusive practices by debt collectors. You have the right to request verification of the debt, dispute it if necessary, and send a cease and desist letter to stop communications.

The Bottom Line

True Accord’s debt collection practices have stirred a mix of experiences, with some users praising their efficiency and others vehemently condemning their methods. While the Better Business Bureau recognizes TrueAccord as a legitimate business, user reviews and complaints highlight potential issues with accuracy, harassment, and confusion.

Navigating the realm of debt collection demands a keen awareness of your rights, a discerning eye for potential scams, and a proactive approach to protect your financial interests. By understanding your rights under the Fair Debt Collection Practices Act, recognizing phishing red flags, and taking informed action, you can safeguard yourself from deceptive practices in the debt collection industry.

In summary, whether TrueAccord is a legitimate debt collection agency or part of a potential scam requires careful consideration of user experiences and official recognition. By staying informed and proactive, you can navigate the complex landscape of debt collection with confidence, ensuring that your rights are upheld and your financial well-being is protected.

Thanks for the insight and useful information